You love your business, but that doesn’t mean you can afford to work for free. Yet, figuring out how to pay yourself as a business owner can be complicated.

You need to think carefully about how you take money out of your business entity. Typically, that’s done one of two ways: a salary or an owner’s draw.

Let’s look at a salary vs. draw, and how you can figure out which is the right choice for you and your business.

Owner’s Draw or Salary: How to Pay YourselfSome business owners pay themselves a salary, while others compensate themselves with an owner’s draw. But how do you know which one (or both) is an option for your business? Follow these steps.

Step #1: Understand the Difference Between Salary Vs. DrawBefore you can decide which method is best for you, you need to understand the basics. Here’s a high-level look at the difference between a salary and an owner’s draw (or simply, a draw):

Owner’s Draw: The business owner takes funds out of the business for personal use. Draws can happen at regular intervals, or when needed.Salary: The business owner determines a set wage or amount of money for themselves, and then cuts a paycheck for themselves every pay period.Those are the nuts and bolts, but we’ll dig into even more details of salaries and draw in a later section.

Step #2: Understand How Business Classification Impacts Your DecisionThere are a lot of factors that will influence your choice between a salary, draw, or another payment method (like dividends), but your business classification is the biggest one. The main types of business entities include:

C Corporation (C Corp)S Corporation (S Corp)Sole ProprietorshipLimited Liability Company (LLC)PartnershipWhy does this matter? Because different business structures have different rules for the business owner’s compensation. For example, if your business is a partnership, you can’t earn a salary because the IRS says you can’t be both a partner and an employee.

(We have an entire section below that breaks down the different business classifications and the best way for each business owner to pay themselves.)

Step #3: Understand How Owner’s Equity Factors Into Your Decision“Owner’s equity” is a term you’ll hear frequently when considering whether to take a salary or a draw from your business. Accountants define equity as the remaining value invested into a business after all liabilities have been deducted.

When you contribute cash, equipment, and assets to your business, you’re given equity—another term for ownership—in your business entity, which means you’re able to take money out of the business each year.

It’s important to understand your equity because if you choose to take a draw, your total draw can’t exceed your total owner’s equity.

Step #4: Understand Tax and Compliance ImplicationsIn addition to the different rules for how various business entities allow business owners to pay themselves, there are also various tax implications to consider.

With regard to taxes, C Corps are different from all other types of business entities. Here’s how:

C Corporations: C Corps are subject to double taxation. The C Corp files a tax return and pays taxes on net income (profit).Pass-Through Entities: Generally, all other business structures pass the company profits and losses directly to the owners. That’s why they’re referred to as pass-through entities.Step #5: Determine How Much to Pay YourselfThere’s a lot that goes into figuring out how to pay yourself. But here’s your next question: How much should you pay yourself?

There’s not one answer or formula that applies across the board. You’ll need to take the following factors into account:

Business structureBusiness performanceBusiness growthReasonable compensationPersonal needsStep #6: Choose Salary Vs. Draw to Pay YourselfOnce you’ve considered all of the above factors, you’re ready to determine whether to pay yourself with a salary, draw, or a combination of both.

You’ll also have a better understanding of how much compensation you’re realistically able to take out of your business.

Understanding the Difference Between an Owner’s Draw and a SalaryWe’ve covered the difference between an owner’s draw and a salary at a high level, but now let’s take a look at the nitty-gritty details of each, using an example: Patty, who is a sole proprietor and owns a catering company called Riverside Catering.

What Is an Owner’s Draw?An owner’s draw refers to an owner taking funds out of the business for personal use. Many small business owners compensate themselves using a draw, rather than paying themselves a salary.

Patty could withdraw profits generated by her business or take out funds that she previously contributed to her company. She may also take out a combination of profits and capital she previously contributed.

Because Patty is a sole proprietor, all of the income earned by her business will show up on her personal tax return and she’ll need to pay estimated tax payments and self-employment taxes on those earnings.

She doesn’t pay separate taxes on the owner’s draw because she’s simply taking out money that has been taxed in the past (which reduces equity) or money that will be taxed in the current year.

Pros and Cons of an Owner’s DrawPro:

Greater flexibility: Rather than needing to pay herself a set amount, Patty’s compensation can fluctuate depending on how her business is performing.Con:

Reduced funds: An owner’s draw reduces a business’s equity, which reduces the funds available for future business spending.What is a salary?You probably already understand what a salary is: You get paid a set amount every pay period. It works really similarly when you’re the business owner. You determine your reasonable compensation and give yourself a paycheck every pay period.

For example, maybe instead of being a sole proprietor, Patty set up Riverside Catering as an S Corp. She has decided to give herself a salary of $50,000 out of her catering business. From there, she could do the math to determine what her paycheck should be given her current pay schedule.

Pros and cons of a salaryPro:

Less Admin Work: Taxes are deducted from your paycheck automatically. Additionally, your compensation as the business owner is a more stable expense, which makes it easier to track your income and expenses.Con:

Cash Flow: What happens if your business has a down month? While it’s possible to adjust your salary to give yourself some more wiggle room, your salary still needs to fall within the IRS’ definition of reasonable compensation. Plus, figuring out how much to pay yourself can be challenging.Business Taxations to ConsiderBefore you make the owner’s draw vs. salary decision, you need to form your business.

There are many ways to structure your company, and the best way to understand the differences is to consider C Corps vs. all other business structures:

Corporations: The C Corp files a tax return and pays taxes on net income (profit). The owners can retain the after-tax earnings for use in the business, or pay shareholders a cash dividend. If a dividend is paid, the dividend income is added to other sources of income on the shareholder’s personal tax return.Pass-through entities: Generally, all other business structures pass the company profits and losses directly to the owners. Sole proprietorships, partnerships, S Corps, and several other businesses are referred to as pass-through entities. Assume, for example, that Patty’s catering business is a partnership and her share of the income is $10,000. The partnership would file a tax return and issue her a Schedule K-1, which reports the $10,000 in income. The $10,000 is then reported on her personal tax return as income from her partnership. The partnership tax return documents the partners, the percentages of ownership, and the partnership’s profit—but no taxes are actually calculated on the partnership tax return.There are some exceptions, but generally, a business faces double taxation as a C Corp. If not, the company is a pass-through entity.

Understanding Owner’s EquityOnce you form a business, you’ll contribute cash, equipment, and other assets to the business. When you contribute assets, you are given equity (ownership) in the entity, and you may also take money out of the business each year. To make the salary vs. draw decision, you need to understand the concept of owner’s equity.

What’s equity? To put it simply, it’s an accumulation of money that has not been spent on the business or withdrawn overtime for personal use. Equity is based on the balance sheet formula:

Assets — Liabilities = Equity

Assets are resources used in the business, such as cash, equipment, and inventory. Liabilities, on the other hand, are obligations owed by the business. Accounts payable, representing bills you must pay every month, are liability accounts, as are any long-term debts owed by the business.

If a company sells all of its assets for cash and then uses the cash to pay all liabilities, any cash remaining in the firm’s equity.

Each owner can calculate his or her equity balance, and the owner’s equity balance may have an impact on the salary vs. draw decision.

Paying Yourself By Business Type or ClassificationForgive us for sounding like a broken record, but the biggest thing you need to consider when figuring out how to pay yourself as a business owner is your business classification.

Why does this matter? Well, because many business entities don’t allow you to take a salary. Let’s take a look at each type of business entity and how this impacts the salary vs. draw decision.

Paying Yourself as a Sole ProprietorPayment Method: Owner’s draw

A sole proprietor’s equity balance is increased by capital contributions and business profits and is reduced by the owner’s draws and business losses.

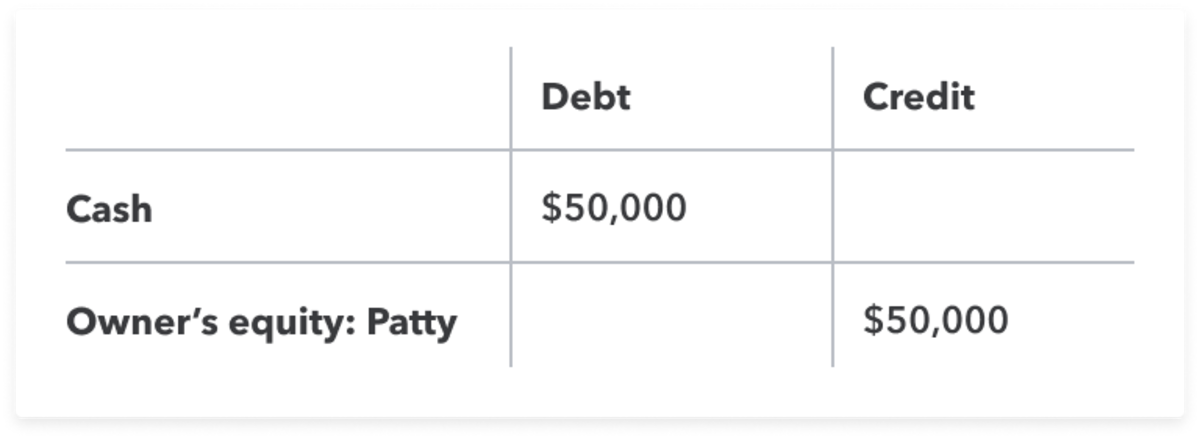

Let’s go back to Patty and her Riverside Catering business. In this example, Patty is a sole proprietor and she contributed $50,000 when the business was formed at the beginning of the year. Riverside Catering posts this entry to record Patty’s capital contribution:

A normal balance for an equity account is a credit balance, so Patty’s owner equity account has a beginning balance of $50,000. During the year, Riverside Catering generates $30,000 in profits. Since Patty is the only owner, her owner’s equity account increases by $30,000 to $80,000. The $30,000 profit is also posted as income on Patty’s personal income tax return.

Patty can choose to take an owner’s draw at any time. She could choose to take some or even all of her $80,000 owner’s equity balance out of the business, and the draw amount would reduce her equity balance. So, if she chose to draw $40,000, her owner’s equity would now be $40,000.

Keep in mind that Patty pays taxes on the $30,000 profit, regardless of how much of a draw she takes out of the business.

Paying Yourself In a PartnershipPayment Method: Owner’s draw

A partners’ equity balance is increased by capital contributions and business profits, and reduced by partner (owner) draws and business losses.

Patty not only owns her catering business, but she’s also a partner in Alpine Wines, a wine and liquor distributor. Patty and Susie each own 50% of Alpine Wines, and their partnership agreement dictates that partnership profits are shared equally. Patty contributes $70,000 to the partnership when the business is formed, and Alpine Wines posts this journal entry:

The partnership generates $60,000 profit in year one, and $30,000 of the profit is reported to Patty on Schedule K-1. Patty includes the K-1 on her personal tax return and pays income taxes on the $30,000 share of partnership profits. Assume that Patty decides to take a draw of $15,000 at the end of the year. Here is her partner equity balance after these transactions:

$70,000 contributions + $30,000 share of profits – $15,000 owner’s draw = $85,000 partner equity balance

Keep in mind that a partner can’t be paid a salary, but a partner may be paid a guaranteed payment for services rendered to the partnership. Like a salary, a guaranteed payment is reported to the partner, and the partner pays income tax on the payment. The partnership’s profit is lowered by the dollar amount of any guaranteed payments.

Paying Yourself From a Limited Liability Company (LLC)Payment Method: Owner’s draw

You must form an LLC according to your state’s laws, and the rules for LLCs differ slightly by state.

In the eyes of the IRS, an LLC can be taxed as a sole proprietorship, a partnership, or a corporation. The rules explained above will apply to how Patty should pay herself as an LLC if she’s taxed as a sole proprietor or partnership.

Paying Yourself as an S CorpPayment Method: Salary and distributions

If Patty’s catering company were set up as an S Corp, then she would figure out a reasonable compensation for the type of work she does and pay herself a salary. To not raise any red flags with the IRS, her salary should be similar to what people in similar positions at other businesses earn. She’ll also need to withhold taxes from her paychecks.

However, to avoid withholding self-employment taxes on the whole amount, Patty could also take a portion of her compensation as a distribution. Distributions are from earnings that were previously taxed at her personal rate. Keep in mind that Patty also needs to have enough equity to take distributions.

For example, if Patty wishes to be paid $75,000 from her business, she might take $50,000 as a salary and distributions of $25,000.

Paying Yourself From a CorporationPayment Method: Salary and dividends

Owners of a corporation are called shareholders. Let’s say that Patty’s catering company is a corporation, but she’s the only shareholder. She must pay herself a salary based on her reasonable compensation.

However, she can also receive a dividend, which is a distribution of her company’s profits. That dividend would be taxed on her personal tax return.

Keep in mind that her business doesn’t have to pay a dividend. She could choose to have the business retain some or all of the earnings and not pay a dividend at all.

Other Considerations for Paying Yourself as a Business OwnerFiguring out how to pay yourself as a business owner can be complicated. Here are a few other things you’ll want to keep in mind when deciding between a salary and a draw.

Social Security and Medicare TaxesSocial Security and Medicare taxes (known together as FICA taxes) are collected from both salaries and draws.

Sole proprietors and partners in a partnership each pay self-employment taxes on profits earned by the company. The self-employment tax collects Social Security and Medicare contributions from these business owners. If instead, a salary is paid, the owner receives a W-2 and pays Social Security and Medicare taxes through wage withholdings.

In contrast, S Corp shareholders do not pay self-employment taxes on distributions to owners, but each owner who works as an employee must be paid a reasonable salary before profits are paid. Remember, the IRS has guidelines that define what a reasonable salary is, based on work experience and job responsibilities.

Risks of Taking Large DrawsIt’s possible to take a very large draw as the business owner. The business owner may pay taxes on his or her share of company earnings and then take a draw that is larger than the current year’s earning share. In fact, an owner can take a draw of all contributions and earnings from prior years.

However, that isn’t without its risks. If the owner’s draw is too large, the business may not have sufficient capital to operate going forward.

Say, for example, that Patty has accumulated a $120,000 owner equity balance in Riverside Catering. Her equity balance includes her original $50,000 contribution and five years of accumulated earnings that were left in the business.

If Patty takes a $100,000 owner’s draw right now, her catering company may not have enough money to pay for employees’ salaries, food costs, and other business expenses.

Avoiding Tax ConfusionDepending on your business structure, you might be able to pay yourself a salary and take an additional payment as a draw, based on profit for the previous year. Make sure you plan carefully to pay your tax liability on time in order to avoid penalties and be payroll compliant.

In addition, to stay organized and payroll compliant, it is recommended to keep payroll records for about six years.

Online payroll services will help you keep your payroll tax documents organized. Choosing the right provider, one that supplies expert support, will be key in assisting with any tax confusion or compliance issues.

How to Determine How Much to Pay Yourself as a Business OwnerMaybe you’ve made the decision between a salary and a draw, but now you’re not sure how much you should be taking out of the business for yourself.

As we mentioned earlier, there isn’t one answer that applies to all business owners. Data from Payscale shows that the average business owner makes $70,220 per year. But, many business owners don’t take a salary in the first few years.

Here are a few things that you should consider as you’re crunching the numbers:

Business structure: Your business entity impacts a lot of your decisions. Many entities don’t allow you to take a salary, meaning you’ll need to take an owner’s draw.Business performance: Regardless of which way you choose to pay yourself, it’s important to remember that your compensation as the business owner isn’t set in stone. You can make some changes as you consider your business’s performance. You should only pay yourself from your profits and not overall revenue. So, if your business is doing well, you might be able to increase your compensation.Business growth: While performance is an important consideration, so is the current stage of your business. For example, if your business is a relatively new startup and in a stage of high growth, you’ll likely want to reinvest a lot of the profits back into the business, rather than pocketing them as compensation for yourself.Reasonable compensation: Only taking a $10,000 salary from your company each year is going to raise some red flags with the IRS. Make sure you familiarize yourself with the IRS’ guidelines and ask around to figure out what a reasonable salary for your type of work is.Personal expenses: That reasonable compensation will give you a starting point, but it doesn’t need to be your only answer. You have personal expenses—from your mortgage or rent to your savings account—that you need to fund. Get a good grasp on what those expenses are, so you can make sure you’re taking home enough to cover them.Those considerations will help you land on a suitable number to pay yourself, whether you take it as a salary or a draw.

Which Method Is Right for You? Salary Vs. DrawYour business entity will be the biggest determining factor in whether you take a salary or draw (or both). For example, if your business is a partnership, you can’t take a salary—you have to take an owner’s draw.

So, make sure that you review the above section on business classifications carefully as that will reveal a lot about the best way to pay yourself as a business owner.

Here are a few other things to consider:

Business Funding: You need to leave enough capital in the business to operate, so consider that before you take a draw.Tax Liability: A business owner needs to be very clear about the tax liability incurred, whether the distribution is a salary or a draw. Work with a CPA to plan for your tax liability and any required estimated payments.Each Method Generates a Tax Bill: You’ll pay Social Security, Medicare, and income taxes through each type of business entity. Your decision about a salary or owner’s draw should be based on the capital your business needs and your ability to perform accurate tax planning.This decision regarding a salary or a draw impacts your business and your personal tax liability.

Paying Yourself In QuickBooksPaying yourself an owner’s draw in QuickBooks is easy. Watch the short video below to get a step-by-step walkthrough.

Pay Yourself the Right WayYou have a lot of love for your business, but you also know that love doesn’t pay your bills. As the business owner, you need to pay yourself to cover your personal expenses and justify the time you spend working in your business.

But, of course, compensating yourself isn’t always straightforward. Use this article as your guide to determine whether you should take a salary or a draw, as well as how much you should reasonably pay yourself.

That way, you can get what you deserve—without risking the financial health and compliance of your business.

To Find Out More About QuickBooks Payroll, Click Here

This content is for information purposes only and should not be considered legal, accounting, or tax advice, or a substitute for obtaining such advice specific to your business. Additional information and exceptions may apply. Applicable laws may vary by state or locality. No assurance is given that the information is comprehensive in its coverage or that it is suitable in dealing with a customer’s particular situation. Intuit Inc. does not have any responsibility for updating or revising any information presented herein. Accordingly, the information provided should not be relied upon as a substitute for independent research. Intuit Inc. does not warrant that the material contained herein will continue to be accurate nor that it is completely free of errors when published. Readers should verify statements before relying on them.

We provide third-party links as a convenience and for informational purposes only. Intuit does not endorse or approve these products and services, or the opinions of these corporations or organizations, or individuals. Intuit accepts no responsibility for the accuracy, legality, or content on these sites.