Time is running out for tax-filers, with the deadline to file your taxes by April 18, 2022. In the video above, Lisa Greene-Lewis, a certified public account (CPA) and TurboTax expert, gives some advice to new investors on cryptocurrency, self-employed taxes, the Child Tax Credit, and more.

Advice for New Investors:Taxable transactions. You don’t have a taxable event until you sell your stock or crypto, or trade your crypto.How you’re taxed. You’re taxed based on how long you hold your stocks or crypto before you sell them. If you hold your stock or crypto for over a year, then you have the benefit of long-term capital gains.Losses. If you had any losing stock or crypto losses when you sold, you can offset your gains with those losses. And your losses can carry over to your ordinary income like W-2 income or self-employment income, up to $3,000.Biggest Tax Mistakes for Gen Z & MillennialsNot filing at all. A lot of millennials and Gen Z may work a job that doesn’t meet the income thresholds for IRS to require them to file. They could be missing out on a tax refund if they had federal taxes withheld that they can get back and education credits, and the third stimulus that they can claim.Gathering documents. Gather all forms that report income like W-2s and 1099s.Education credits. They may be eligible for the American Opportunity Credit if they were in their first four years of college, or the Lifetime Learning Credit, even if they were taking just one class.Related: Child Tax Credit – What You Need to Know (Video)

The Child Tax Credit Explained17 and under. Under the new Child Tax Credit expansion in 2021, you are able to get the credit if your child is 17 and under. Previously, you were not able to get this credit for your child if they were 17.Income limit. The income limit is $75,000 if you’re filing single, and under $150,000 if you’re married filing jointly. The credit is phased out for incomes over those amounts.Advanced payments. Once you file your tax returns, you’re going to have to put in the dollar amount of advances that you received. Because it was an advance, you will probably see a lower Child Tax Credit than you’re used to, and possibly a lower tax refund.IRS letter 6419. Make sure that you have the new letter that the IRS is issuing. You want to make sure to hold onto that letter for filing your taxes and to make sure that information is correct.Related: Child Tax Credit (2021-2022) Explained and What It Means for Your Taxes

Quotes | 2022 Tax Deadline Looms: Everything You Need to KnowLisa Greene-LewisCertified public accountant and TurboTax Expert

Full Video Transcript Below:Tracy Byrnes: While on one hand, it’s very cool to be entrepreneurial, on the other hand, a lot of this paperwork now falls into your lap, right?

Lisa Greene-Lewis: If your net income is $400 or more, then you need to file a tax return because you have to pay self-employment taxes. For most self-employed jobs, you might drive your car for your business. You can deduct your car, either your mileage or your actual expenses.

Related: 5 Pandemic-Related Tax Questions Answered

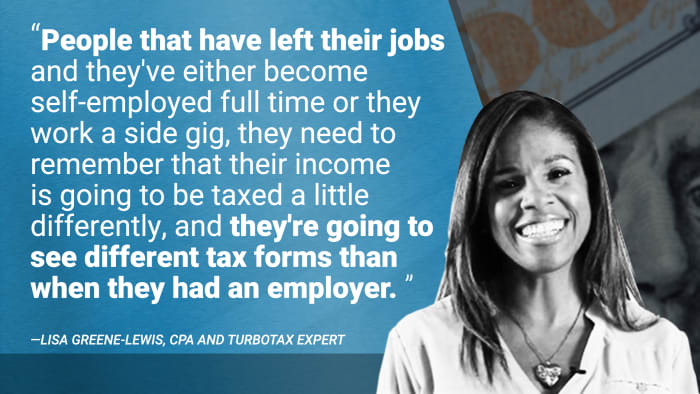

People that have left their jobs and they’ve either become self-employed full-time or they work a side gig, need to remember that their income is going to be taxed a little differently. And they’re going to see different tax forms than when they had an employer.

The Child Tax Credit was huge, they expanded it, and now it’s increased to up to $3,600 for each of your children under six. Under the new Child Tax Credit expansion, you’re able to get the credit if your child is 17 and under.

People don’t even know when their transactions are taxable. You don’t have a taxable event until you sell your stock or crypto. Also, depending on how long you hold your stocks before your sell them, that’s also how you’re taxed. Remember, if you had any losing stock or crypto losses, you can offset your gains with those losses. And then your losses can carry over to your ordinary income, and that’s up to $3,000.

One of the biggest mistakes that millennials and Gen Z make, a lot of them, not filing at all.

More tax advice from TurboTax’s Lisa Greene-Lewis:Tax Tips for Those Joining the Great Resignation3 Biggest Tax Mistakes Made by Gen Z and MillennialsCrypto Tax Guide to Capital Gains and LossesEditor’s note: Video produced by TheStreet’s Justin Ho.