Amazon.com’s (AMZN, $109.22) Prime Day is upon us once again. Alas, the frenzy of savings, discounts and deals on millions of items offered by the e-commerce giant is open only to Amazon Prime subscribers.

Happily for investors, however, AMZN stock is as much on sale as anything to be found on the retailer’s website (which right now, includes everything from Apple watches to security cameras, or Crocs to car seats). Absolutely everyone is invited to pick it up.

And most importantly, if analysts are correct, bargains like this don’t come along very often.

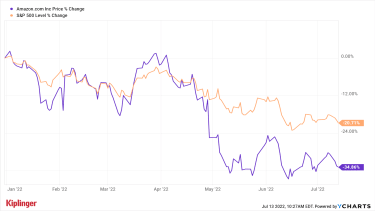

Here’s how AMZN stock became such a hot Amazon Prime Day deal. Shares are off by 35% for the year-to-date, lagging the broader market by about 15 percentage points. Rising fears of recession and its potential impact on retail spending are partly responsible for the selloff. The market’s rotation out of pricey growth stocks and into more value-oriented names is likewise doing AMZN no favors. See the chart below:

AMZN stock Amazon Prime Day

True, Amazon is hardly alone when it comes to mega-cap names getting slaughtered in 2022. Where the stock does distinguish itself is in its deeply discounted valuation, and the mass of Wall Street analysts banging the table for it as a screaming bargain buy.

AMZN’s Elite Consensus RecommendationIt’s well known that Sell calls are rare on the Street. For different reasons entirely, it’s almost equally unusual for analysts (as a group, anyway) to bestow uninhibited praise on a name. Indeed, only 25 stocks in the S&P 500 carry a consensus recommendation of Strong Buy.

AMZN happens to be one of them. Of the 53 analysts issuing opinions on the stock tracked by S&P Global Market Intelligence, 37 rate it at Strong Buy, 13 say Buy, one has it at Hold, one says Sell and one says Strong Sell.

If there is a single point of agreement among the many, many AMZN bulls, it’s that shares have been beaten down past the point of reason.

Here’s perhaps the best example of that disconnect: At current levels, Amazon’s cloud-computing business alone is worth more than the value the market is assigning to the entire company.

Just look at Amazon’s enterprise value, or its theoretical takeout price that accounts for both cash and debt. It stands at $1.09 trillion. Meanwhile, Amazon Web Services – the company’s fast-growing cloud-computing business – has an estimated enterprise value by itself of $1.2 trillion to $2 trillion, analysts say.

In other words, if you buy AMZN stock at current levels, you’re getting the retail business essentially for free. True, AWS and Amazon’s advertising services business are the company’s shining stars, generating outsized growth rates. But retail still accounts for more than half of the company’s total sales.

More traditional valuation metrics tell much the same story with AMZN stock. Shares change hands at 42 times analysts’ 2023 earnings per share estimate, according to data from YCharts. And yet AMZN has traded at an average forward P/E of 147 over the past five years.

Paying 42-times expected earnings might not sound like a bargain on the face of it. But then few companies are forecast to generate average annual EPS growth of more than 40% over the next three to five years. Amazon is. Combine those two estimates, and AMZN offers far better value than the S&P 500.

Analysts Say AMZN Is Primed for OutperformanceBe forewarned that as compellingly priced as AMZN stock might be, valuation is pretty unhelpful as a timing tool. Investors committing fresh capital to the stock should be prepared to be patient.

That said, the Street’s collective bullishness suggests AMZN investors won’t have to wait too long to enjoy some truly outsized returns. With an average target price of $175.12, analysts give AMZN stock implied upside of a whopping 60% in the next 12 months or so.

Kiplinger is supported by its audience. When you purchase through links on our site, we may earn an affiliate commission. Read about our editorial standards.