There is an old joke that some statisticians tell, that “a person with their head in an oven and their feet in the freezer is comfortable — on average.” Statisticians are not known for their sense of humor (clearly), but the joke is an effective warning about some of the shortcomings of relying on averages.

Statistically, a simple average camouflages extremes within its sample data. And, while the statistician’s joke is somewhat extreme, it is no less extreme than the actual returns in the long-run average annual returns for stocks and bonds that set many investors’ return expectations.

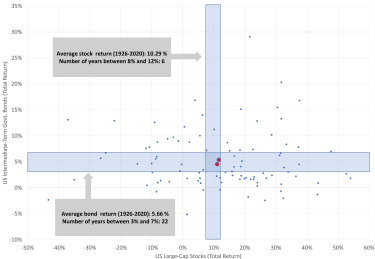

What’s an ‘average’ annual return anyway?If quizzed, it is likely that many investors would estimate the average annualized returns for U.S. stocks and bonds to be about 10% and 5%, respectively. Those averages are composed of decades of returns and describe history perfectly. However, although they describe the average annualized returns, they are a far cry from the typical or “average” experience. In fact, in only two years from 1926 through 2020 did both the stock and bond market deliver returns within 2% (+/-) of their historical averages (see Figure 1).

Figure 1: Annual stock and bond returns, 1926-2020In 2021, U.S. stocks gained 25.7%, while U.S. bonds lost 1.5%.* While it is fair to say that it was a great year for stocks, is it fair to say that it was a bad year for bonds because they didn’t return their 5.7%* average? Probably not. The only thing rarer than a year with “average” returns might be a year that investors appreciate their bond allocations amid a bull market for stocks.

For those of you thinking about abandoning bonds, here are some ideas that may help:

A bad day for stocks is often much worse than a bad year for bonds.While investors prefer gains to losses, they also prefer small losses to big losses. While far from being predictive, Figure 1 demonstrates that negative returns in bonds have tended to be both infrequent and modest. In fact, the bond market’s worst annual return was a loss of 5.1% in 1994. However, the stocks of the S&P 500 index have posted daily losses that bad or worse 25 times since 1926.

Sometimes, the further the distance, the clearer the picture.Often, it’s hard for investors to see the benefits that high-quality bonds can add to their portfolios, especially when the returns they are posting are modest — or even modestly negative. And today, concerns for higher interest rates due to higher-than-expected inflation are making it even more challenging for investors to ignore some pundits’ suggestions that holding bonds is a bad idea.

I was given a magnifying glass when I was young, and I started looking at everything through it. Eventually, I looked at the Sunday comics and realized that for all I saw, I wasn’t seeing everything. The cartoons were nothing but a variety of colored dots! Magazine photos, too. It made me wonder how much else I was missing because I wasn’t looking closely enough. Now, I realize that when I was close enough to see the dots, I missed the bigger picture – literally.

Similarly, the dots in Figure 1 paint a picture that’s easy to overlook when you’re too narrowly focused: The principal benefit of investment-grade bonds isn’t their frequency of positive returns but the infrequency of large, negative returns. And, yes, if the returns in Figure 1 were inflation-adjusted, the frequency of negative returns for both bonds and stocks would increase. However, that would not change what Figure 1 tells us: High-quality bonds in a portfolio can help moderate the volatility of stocks.

The bottom line: Keep your eye on the big picture.A well-diversified portfolio can benefit from bonds: More likely than not, a bad year for bonds will be much better than a bad day for stocks. While that certainly won’t insure your portfolio against losses, it can certainly help moderate the losses when the markets turn intemperate.

Having a well-diversified portfolio that includes an allocation to high-quality bonds can help keep a bad day in the stock market from turning into a bad year for your portfolio.

* Stock performance as measured by the CRSP U.S. Total Market Index. Bond performance as measured by the Bloomberg U.S. Aggregate Float Adjusted Index. Bond average is a geometric mean return for the Ibbotson® SBBI® U.S. Intermediate-term (5-Year) Government Bonds (Total return).

This article was written by and presents the views of our contributing adviser, not the Kiplinger editorial staff. You can check adviser records with the SEC or with FINRA.

Don Bennyhoff, CFA®Investment Committee Chairman & Director of Investor Education, Portfolio Solutions

Don Bennyhoff, CFA®, serves as the Chairman of the Investment Committee and Director of Investor Education at Portfolio Solutions, a $1.6B RIA. An industry expert who spent over 22 years at The Vanguard Group, Don was a Founding Member of Vanguard’s Investment Strategy Group, and served as a Senior Investment Strategist.