Earnings revisions, which have served as a key source of support, have turned negative. We anticipate more downside in the months ahead

A trader works on the floor of the New York Stock Exchange. Photo by Spencer Platt/Getty Images By David Rosenberg and Brendan Livingstone

Advertisement 2 This advertisement has not loaded yet, but your article continues below.

Earnings revisions were a key tailwind off the March 2020 stock market low, but are now transitioning towards a headwind, which has negative implications for investors since S&P 500 returns historically have closely tracked the earnings revision ratio.

There are a number of factors behind the negative trend to earnings revisions of late: a slowing global economy; the United States Federal Reserve’s push to remove accommodation; the Russia-Ukraine war; a stronger U.S. dollar; and margin pressure due to rapidly increasing input costs.

Against this backdrop, we believe investors should focus on companies/sectors with limited earnings variability. As a general rule, this means an emphasis on defensives (such as utilities, health care, consumer staples and real estate) versus cyclicals.

Advertisement 3 This advertisement has not loaded yet, but your article continues below.

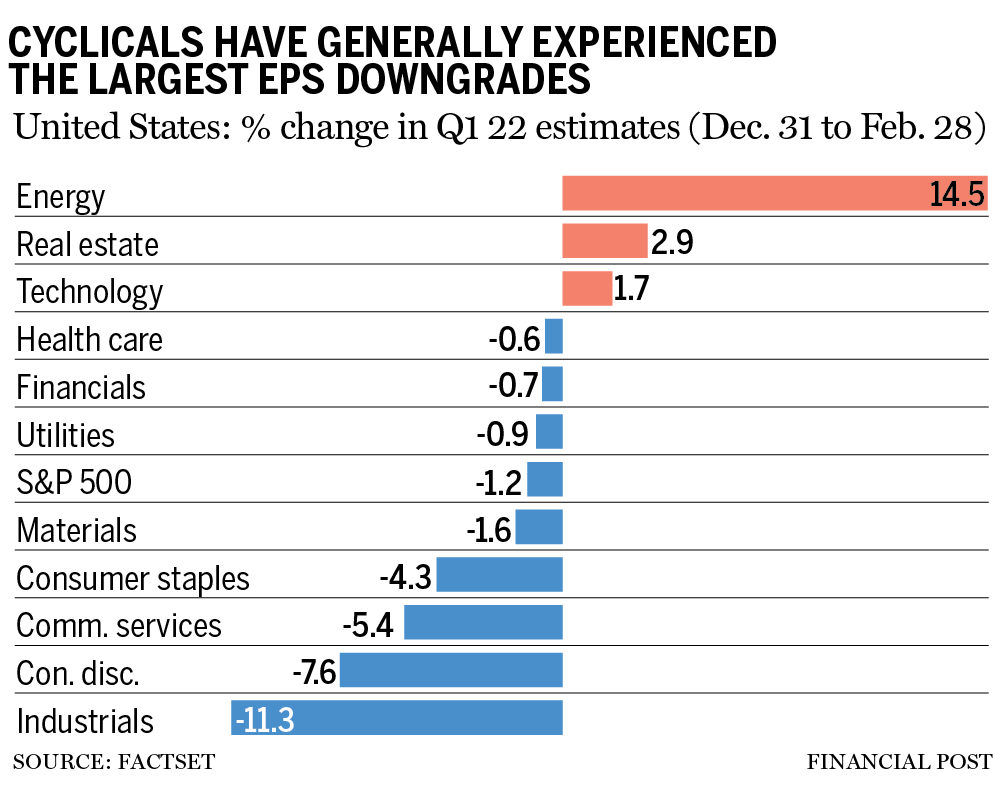

Indeed, earnings data for the first quarter lends support to our call for defensives over cyclicals. Between Dec. 31, 2021, and Feb. 28, 2022, Q1 2022 EPS estimates for the S&P 500 were revised lower by 1.2 per cent, according to FactSet. Note that this revision would have been even more negative if not for a massive positive revision to energy (14.5 per cent) on account of the continued surge in oil prices.

Eight of 11 sectors had earnings downgrades over the past two months. Besides energy, the only other positive exceptions were real estate (2.9 per cent) and technology (1.7 per cent). Conversely, industrials (11.3 per cent) and consumer discretionary (7.6 per cent) — classic cyclical sectors — as well as communication services (5.4 per cent) had the largest negative revisions.

Advertisement 4 This advertisement has not loaded yet, but your article continues below.

The average EPS revision for defensive sectors — real estate, health care, utilities and consumer staples — is -0.7 per cent thus far for Q1. This is a smaller downgrade than the S&P 500 (-1.2 per cent) as a whole, and is a good illustration of their far more limited earnings variability.

In contrast, the average EPS revision for cyclical sectors — financials, materials, consumer discretionary and industrials — is -5.3 per cent. Looking ahead, we continue to see more downside in EPS estimates, particularly in cyclicals.

Depending on the extent of the future hit to earnings estimates, this will offset some of the positive impact on valuations from the current selloff in equities. Put differently, if the “E” (earnings) in P/E ratios is adjusted downward, it will take a larger fall in the “P” (prices) to return valuations towards attractive levels.

Advertisement 5 This advertisement has not loaded yet, but your article continues below.

Therefore, investors thinking about good entry points should adjust current EPS estimates (which are stale) lower in the interest of being conservative and preparing for future earnings downgrades.

One final point: our “earnings revision breadth tracker” — which captures the net share of S&P 500 industries with positive earnings revisions on a 13-week rolling average basis — is well off its nearby peak. Currently, this metric is at 61 per cent, which is above average historically, but considerably less than peak levels (90 per cent) in early 2021. In essence, we are moving from an environment where earnings revisions were historically strong to one that more closely resembles an “average” backdrop.

More On This Topic David Rosenberg: Looking for opportunities amidst the volatility David Rosenberg: The Russians aren’t coming, they’ve arrived — here’s what could happen next David Rosenberg: How key asset classes performed following a yield curve inversion David Rosenberg: Global recovery unhealthily hitched to bubbly housing, especially in Canada, New Zealand This advertisement has not loaded yet, but your article continues below.

Article content The bottom line is that earnings revisions, which have served as a key source of support, have turned negative. We anticipate more downside in the months ahead as analysts confront the reality of a very challenging economic backdrop. With this in mind, we expect the major equity indexes to continue to struggle since there has been a tight historical correlation between the earnings revision ratio and stock-market returns.

However, there are segments where investors can hide, mainly in defensive sectors where earnings exhibit less variability. In addition, energy, which has had large upward revisions of late, is another good option as long as oil prices continue to rise.

David Rosenberg is founder of independent research firm Rosenberg Research & Associates Inc. Brendan Livingstone is a senior strategist there. You can sign up for a free, one-month trial on Rosenberg’s website.

_____________________________________________________________

For more stories like this one, sign up for the FP Investor newsletter.

______________________________________________________________

Financial Post Top Stories Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300