The stock market can be a scary place. Our unprecedented bull market run has finally run itself into the ground, and investors are now facing a new reality. Interest rates are rising, inflation is skyrocketing and stocks and bonds are down.

Some investors are reacting with panic, while others are seeing it as more of an opportunity.

How should you deal with today’s bear market? We asked a wide range of experienced financial professionals that very question, and here are their top bear market tips.

1 of 10

Nick Toman: How to react largely depends how close to retirement you areGetty Images

The current state of the stock market is causing virtually all investors to pause and consider if their current strategies are built to weather this storm. Those who are at least 10-15 years away from needing distributions from their investments AND who are continuing to build wealth through systematic and regular contributions (i.e., 401(k), 403(b), IRA , etc.), most likely won’t need to make any significant changes at this point. However, since my clients are primarily those who are within five to seven years of retirement OR who have recently retired, the advice I give goes beyond “stay the course.”

As a STARTING POINT to a strong retirement blueprint, I encourage pre-retirees to understand two principles:

Your strategies should be specific and customized to you and you alone. Go deeper than just following the lead of co-workers, family and friends when determining what moves to make. Since all families have their own set of unique circumstances when it comes to their wealth (longevity, health, tax status, career enjoyment, too many variables to name here), there really is no one-size-fits-all solution … PERIOD!Income is the “driver” of most retirement plans. Having a retirement budget and knowing exactly how to fund this budget each month is key. If the majority of your income will be coming from predictable sources, such as Social Security and pensions, then you should have more flexibility to avoid “locking in losses” by having to sell investments in this bear market. However, if you have a need for money now that is beyond what your Social Security and pensions will cover, then you should consider using financial tools designed to provide income and principal protection, such as CDs and various types of annuities, for a portion of your wealth.Just few things to consider when evaluating your next steps.

Nicholas Toman, CFP®, is a lead retirement planner and investment adviser with Empowered Financial Management, a firm that specializes in retirement planning for those individuals within five to seven years of retirement or who have recently retired and no longer wish to serve as their own financial adviser.

2 of 10

Paul Sydlansky: Focus on what you can control!Getty Images

No one knows where the market is headed, not even the pros (despite what they tell you)! The market could be headed down for two more months or two more years. Instead of worrying about when the downturn will end, spend time on things you can control.

Here are three items I have recently mentioned to clients to take a closer look at:

Re-evaluate the amount of cash in your emergency account. Any market or economic downturn could mean a greater chance of layoffs and job loss. How many months of expenses do you have saved in cash? Are those expenses current (especially considering our recent spike in prices), and are you comfortable with your ability to find a job before these funds run out?Review your cash flow. Will your income take a dip with a prolonged downturn? Are there any expenses you could cut from everyday spending? Increased cash flow could be used to either pad your emergency account or invest (yes, we want you to invest more, read No. 3).Continue investing. Although it seems counterintuitive to invest now, it’s actually a great time for the long-term investor to put capital to work. You now can buy into a market that is over 20% cheaper than it was six months ago. Why wouldn’t you buy stocks now when they are on sale?Paul Sydlansky, founder of Lake Road Advisors LLC, has worked in the financial services industry for over 20 years. Paul is a CERTIFIED FINANCIAL PLANNER™ and a member of the National Association of Personal Financial Advisors (NAPFA) and the XY Planning Network (XYPN).

3 of 10

Chris Chen: What goes down has ALWAYS gone back upGetty Images

Wanting to get out when the market drops is an emotional decision, one that is difficult to go against – especially when it is not just the stock market that is dropping, but also the bond market (government bonds, safe by reputation, are down over 11% so far this year). We just don’t want to give back any more than we already have, especially when we don’t know how much more markets will drop.

Yet, as you calmly ponder the bear market and its 20%+ stock market correction, remember that markets do go down, and they also go up. From 2016 to 2021, data tells us that 46.71% of trading days were DOWN days.

Yes, that is almost 50%. The other 54.86% trading days from 2016 to 2021 were UP days.

That’s more than 50%.

It is hard when we feel gravity playing tricks with our guts, but look at the data, just for a minute. These days, the stock market may feel like bungee jumping without a rope, but it is much more like a roller coaster: Sure, it feels scary on the way down, but it does bottom out, and then it goes back up.

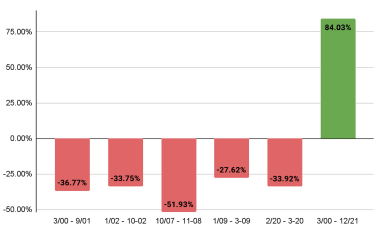

The S&P 500’s Performance since 2000

Courtesy of Chris Chen

We know that because that’s what it has done before.

From March 24, 2000, to Sept. 21, 2001, the S&P 500 dropped 36.77%. From Jan. 4, 2002, to Oct. 9, 2002, it dropped 33.75%. From Oct. 9, 2007, to Nov. 20, 2008, it dropped 51.93%. From Jan. 6, 2009, to March 9, 2009, it dropped 27.62%. From Feb. 19, 2020, to March 23, 2020, it dropped 33.92%Yet, despite all those losses, when you look at the S&P’s performance overall during that entire time frame – from March 24, 2000, to Dec. 31, 2021 – it was up 84.03%.

Will this time be different? Do we have reason to believe that it will? Well, history never repeats itself exactly, but in my opinion, it will rhyme.

Chris Chen, CFP® CDFA, is the founder of Insight Financial Strategists LLC, a fee-only investment advisory firm in Newton, Mass. He specializes in retirement planning and divorce financial planning for professionals and business owners. Chris is a member of the National Association of Personal Financial Advisors (NAPFA).

4 of 10

Eric Roberge: Do what would Warren Buffett would doGetty Images

Resist the temptation to do something just to act. The correct response in dealing with a bear market (this or future ones) may well be to “do nothing” when it comes to your investment portfolio. If you’re a long-term investor, then hopefully you have a comprehensive strategy in place that was designed with the knowledge that down markets WILL happen along the way. If that’s the case, tinkering with your portfolio as a reaction to what’s happening currently is probably a bad move. If you DON’T have a strategy and you feel worried about the market, now may be the time to work with a professional to get that plan in place so you have that (and an adviser!) to guide you when things feel turbulent.

Remember that doing nothing with your investment portfolio doesn’t necessarily mean doing nothing with your finances in general. You can’t control the market, but there are plenty of other aspects of your money that you do have the power to influence. So, think about where you can make an adjustment in an area you have complete control over. The best way to take action may be to:

Decrease your spending.Increase your savings.Focus on building up cash for emergencies.Or put more cash in the market! This is especially pertinent now, when inflation is also running rampant.While you don’t want to lose all your liquidity when economic outlooks feel bleak, there is such a thing as having too much cash on hand. Our guideline for our planning clients is to keep enough cash on hand to cover three to six months’ worth of expenses as an emergency reserve, as well as any cash needed for upcoming, known spending needs or short-term goals. (For example, if you know you want to renovate your home next year and it will cost $50,000, that money should be in cash and available to use toward your goal.)

If you have enough cash for defined short-term goals and your emergency fund, then anything over that amount should be in the market and going to work for you – not sitting in the bank losing purchasing power to inflation.

Now is a great opportunity for long-term investors to buy into the market at lower prices. It can feel scary to jump in when everyone else is fleeing, but that’s one big reason why Warren Buffett is famous: “Be greedy when others are fearful!”

Eric Roberge, CFP®, is the founder of Beyond Your Hammock, a financial planning firm working in Boston and virtually across the country. BYH specializes in helping professionals in their 30s and 40s use their money as a tool to enjoy life today while planning responsibly for tomorrow.

5 of 10

Don Wilson: We’ve got some strategic opportunities now, so take advantageGetty Images

I would encourage investors to review their short-term investments and consider opportunities the rise in rates have created.

Interest rates have risen sharply in a short period of time, giving investors a much better return opportunity on short-term Treasury bonds and certificates of deposit than just a few months ago.

For example, rates have likely increased for people with funds in a money market or a bank account. However, those willing to forgo immediate liquidity can earn substantially higher interest rates by buying Treasuries or certificates of deposits with maturity dates between two months and two years.

As of June 17, the yield on a two-month U.S. Treasury bond was 1.50%, jumping to 3.17% for a two-year bond. Investors may want to create a bond ladder by buying Treasuries or CDs over multiple maturities based on their liquidity needs.

Another tactic is to use this downturn to rebalance your portfolio by selling asset classes that have held up best and buying those classes hardest hit. For example, this could mean selling investments in some commodities and real estate while picking up high-quality stocks that have been hit hard. Use this to bring your portfolio back to its target weights.

Finally, reduce your potential year-end tax bill by selling positions with losses. You can replace these with similar investments or buy them back after 30 days. This move enables investors to offset the taxes owed on capital gains elsewhere in their portfolios. The result is that less of your money goes to taxes and more may stay invested and working for you.

Don Wilson is a partner and the chief investment officer at CI Brightworth. His primary roles are developing the overall investment strategy for client portfolios, leading the investment research and portfolio management team and chairing the Investment Committee.

6 of 10

Brian Skrobonja: Investors need to prepare for bear markets like skydivers do Getty Images

There are two things that should never surprise you: The fact that investing in the stock market has risks of losing money and that when you skydive you free fall from an airplane. These are both certainties. However, what may surprise you is that people jumping from airplanes are often more prepared for what they anticipate will happen than investors are.

People who skydive enjoy the adrenaline-fueled rush of falling to the earth at 120 miles per hour, but you don’t need to experience jumping out of an airplane to know that the most important part of the trip back to earth is having a parachute.

For investors, the possibility of losing money as a result of a market downturn is well known, yet often ignored as they focus on the long-term growth potential of the market. The attitude most often is to simply grin and bear it, but when markets inevitably turn negative, investors are left wishing they had a proverbial parachute.

You see, regardless of how diversified you think you are or how optimistic you are about the market, when the market falls most everything else in the market falls right along with it – and trying to rearrange the chairs on the Titanic by adding more stock market investments isn’t going to fix the problem.

Investors can build their own proverbial parachute for their portfolio by adding private markets, annuities and specially designed life insurance products designed to work synergistically with the stock market. Yes, some of these carry their own set of risks, but by mixing products together you create a proverbial parachute of investments that do not behave in the same way, aren’t impacted by the same things, don’t grow in the same manner and don’t all fall at the same time.

I go into more detail about this in my column “For Real Financial Security, Do NOT Do What Everyone Else is Doing.”

Brian Skrobonja is an author, blogger, podcaster and speaker. He is the founder of St. Louis Mo.-based wealth management firm Skrobonja Financial Group LLC. His goal is to help his audience discover the root of their beliefs about money and challenge them to think differently. Brian is the author of three books, and his Common Sense podcast was named one of the Top 10 by Forbes.

Securities offered through Kalos Capital Inc., Member FINRA/SIPC/MSRB and investment advisory services offered through Kalos Management Inc., an SEC registered Investment Adviser, both located at11525 Park Wood Circle, Alpharetta, GA 30005. Kalos Capital and Kalos Management do not provide tax or legal advice. Skrobonja Financial Group, LLC and Skrobonja Insurance Services, LLC are not an affiliate or subsidiary of Kalos Capital or Kalos Management.7 of 10

Mike Piershale: If you cashed out of stocks out of fear, start easing back inGetty Images

If you’ve panicked and have already gone to cash, or you know you’re about ready to do so, once you get in a cash position start dollar-cost averaging your way back into the market over the next 12 to 18 months. For example, if you panicked and pulled $225,000 out of the market recently, you could start moving roughly $12,500 back in on the same day each month over the next 18 months.

It’s critical to be disciplined to do this every month, especially in the months where the market falls as this gives you an opportunity to buy the shares cheaper.

This strategy removes much of the agonizing decision-making that goes along with trying to time the market to go back in at the best price.

In essence dollar-cost averaging will help you avoid the mistake of moving the money in one lump sum back into the market right before a precipitous drop. And it’s also a lot easier on your emotions to spread your entry point out over 12 to 18 months rather than putting all the money back into the market at one time.

This strategy tends to lower the price that you’ll pay for your investments over time, leading to less of a loss if they continue to decline, and will generate greater gains when the investments start rebounding.

In a similar fashion you should continue contributing on a monthly basis into the market in your 401(k) plan, especially when the market is going down. The vast majority of the time this will help you get an average price on your shares that will be lower compared to someone who gets rattled and discontinues buying shares every time the market drops.

Mike Piershale, ChFC, is president of Piershale Financial Group in Barrington, Ill. He works directly with clients on retirement and estate planning, portfolio management and insurance needs.

8 of 10

Ken Nuss: Retirees and near-retirees need to watch their riskGetty Images

Many older folks approaching or in retirement have far too much of their portfolios exposed to market risk. When you’re young, you have decades to recover from a prolonged bear market. You don’t when you’re retired and withdrawing money for living expenses.

To reduce risk, guarantee principal and earn a solid return, consider allocating a portion of your portfolio to fixed annuities, which come in two types. Both are tax-deferred when held in a nonqualified account.

A fixed indexed annuity (FIA) removes downside market risk and protects your principal while positioning your money to benefit from a future market rebound whenever it happens. It gives you the best opportunity to keep up with high inflation while still protecting your principal. Interest rate gains are linked to market performance and locked in each year and can never be lost in any future market downturn, thus protecting your principal and previously credited amounts.

The upside is limited by caps and participation rates built into the product. They’ve improved substantially in recent months, giving you more growth potential.

You can add an income rider to guarantee future income regardless of what the market might do. Use this strategy rather than the hope that your portfolio will recover and be sufficient to support your retirement. You can call this your “safe money” allocation.

Many FIAs also come with significant upfront bonuses for investors, which can help make up for recent market losses. Before investing, make sure the product is a good fit for your objectives and needs.

FIAs pay fluctuating interest rates. But fixed-rate annuities (multi-year guarantee annuities) pay a set, guaranteed rate of interest for two to 10 years. It’s a simple, straightforward product that resembles a bank CD. Interest rates have improved dramatically in recent months, and you can now earn up to 4.30%.

Retirement-income expert Ken Nuss is the founder and CEO of AnnuityAdvantage, a leading online provider of fixed-rate, fixed-indexed and immediate-income annuities. Interest rates from dozens of insurers are constantly updated on its website at https://www.annuityadvantage.com.

9 of 10

Marguerita Cheng: Stick with sound investing principles during bear marketsGetty Images

Now is not the time to deviate from the good advice and strategies that have worked for investors over the years. My recommendations to investors right now are to stick to the basics:

Stay diversifiedIt is important to include cash, equities and fixed income in your portfolio. How much you allocate to each investment class is a function of your time horizon, your risk tolerance, your tax bracket and your cash flow requirements. Each asset class plays an important role. Having cash provides peace of mind because it is liquid and readily available. It can protect you against market risk or sequence of return risk by not having to liquidate other assets at an inopportune time.

Although you may be seeing red when you log into your portfolio dashboard, including equities in your portfolio is important because they can appreciate at a rate greater than inflation of the long term. So, equities can help address inflation risk and longevity risk.

Higher inflation and rising interest rates have put downward pressure on bond prices. Bonds may lag equities in good years, but they can help provide stability in a portfolio.

Continue to invest through dollar-cost averagingMany investors don’t realize that dollar-cost averaging is what they’re already doing with their 401(k) plans, 529 plans, Roth IRAs & IRAs all along. Don’t stop now.

Understand the distinction between risk tolerance and risk capacityRisk tolerance is a measure of how much risk you are willing to take on. Generally, there are three types of investors: conservative, moderate and aggressive. The level of risk tolerance increases as you move from conservative to aggressive. Factors including age, income, financial goals and psychological and emotional conditions influence your risk tolerance. Risk tolerance is subjective. While there are factors that inform it (age, income, financial goals), they are not determinative, given the role of emotion and psychology.

CFP® professionals define risk tolerance as the amount of risk you can take and still sleep at night. How much risk are you comfortable with? What level of risk won’t keep you awake at night after refreshing the balance on your portfolio dashboard?

Risk capacity may sound similar, but it’s different in an important way. The level of risk you are willing to take is not the same thing as the level of risk you should take. Risk capacity is the measure of the latter. It’s an objective determination of the level of risk you should be taking in your portfolio to achieve your financial goals. Factors like time frame/time horizon, cash flow, income requirements, debt, insurance and liquidity will determine your risk capacity.

Marguerita M. Cheng is CEO at Blue Ocean Global Wealth. She is a CFP® professional, a Chartered Retirement Planning Counselor℠, Retirement Income Certified Professional and a Certified Divorce Financial Analyst. She helps educate the public, policymakers and media about the benefits of competent, ethical financial planning.

10 of 10

Aoifinn Devitt: Shift to assets that provide ‘all-weather’ protection Getty Images

Our goal in portfolio construction is to ensure that our clients build “all-weather” portfolios that are resilient to volatile market conditions. The past few months have presented a hurricane for investors. Selling has been (almost) indiscriminate across U.S. equities, while bonds have had an epically bad start to the year. A strong U.S. dollar has eroded international investments, and in the face of steep inflation simply holding cash has not seemed like such a safe option either.

Our “all-weather” portfolios emphasize diversification into real assets, which traditionally have acted as inflation hedges. Exposure to real estate, infrastructure and other tangible assets that offer an inflation-linked income stream can provide a portfolio with ballast in a rising inflationary environment, while a diversified portfolio of alternatives can add additional sources of return – such as private lending, private equity investing and venture capital.

Although these investments are all linked to the same economy and same dynamics as public investments, their liquidity terms mean they are not marked to market as frequently and do not suffer from the same intra-month volatility.

We have been pleased to see that access to such assets is improving, even for accredited investors. Improved technology platforms, better fee and share class structures and more access to blue chip names have leveled the playing field with institutional investors in this area.

No portfolio is hurricane proof, but our philosophy of preparation and not prediction, and our continuous return to our core principles of investing for the long term, diversification and staying the course according to each client’s investment objective is key to weathering the storm.

Aoifinn Devitt, who has more than two decades of financial experience and a diverse international background, plays an integral role in establishing Moneta’s long-term investment vision and strategies. She aligns Moneta’s investment programs with broader firm goals while also overseeing the research, evaluation and selection of asset classes and investment vehicles.